All Categories

Featured

Table of Contents

The price is set by the insurance provider and can be anywhere from 25% to greater than 100%. (The insurance firm can additionally change the participate rate over the life time of the policy.) If the gain is 6%, the engagement price is 50%, and the present cash money value total is $10,000, $300 is included to the cash money value (6% x 50% x $10,000 = $300).

There are a variety of pros and cons to take into consideration prior to acquiring an IUL policy.: Just like conventional universal life insurance policy, the insurance policy holder can increase their premiums or reduced them in times of hardship.: Quantities attributed to the cash worth grow tax-deferred. The cash money worth can pay the insurance costs, permitting the insurance policy holder to reduce or quit making out-of-pocket costs settlements.

Numerous IUL policies have a later maturation date than other kinds of global life policies, with some ending when the insured reaches age 121 or even more. If the insured is still to life at that time, policies pay out the fatality benefit (however not usually the cash money value) and the proceeds might be taxed.

: Smaller policy face values don't use much benefit over normal UL insurance coverage policies.: If the index decreases, no rate of interest is attributed to the cash worth. (Some policies use a low guaranteed rate over a longer duration.) Various other financial investment automobiles utilize market indexes as a criteria for efficiency.

With IUL, the objective is to make money from higher movements in the index.: Because the insurance provider only acquires options in an index, you're not straight purchased stocks, so you don't profit when companies pay rewards to shareholders.: Insurers cost fees for handling your money, which can drain cash value.

Allstate Futuregrowth Iul

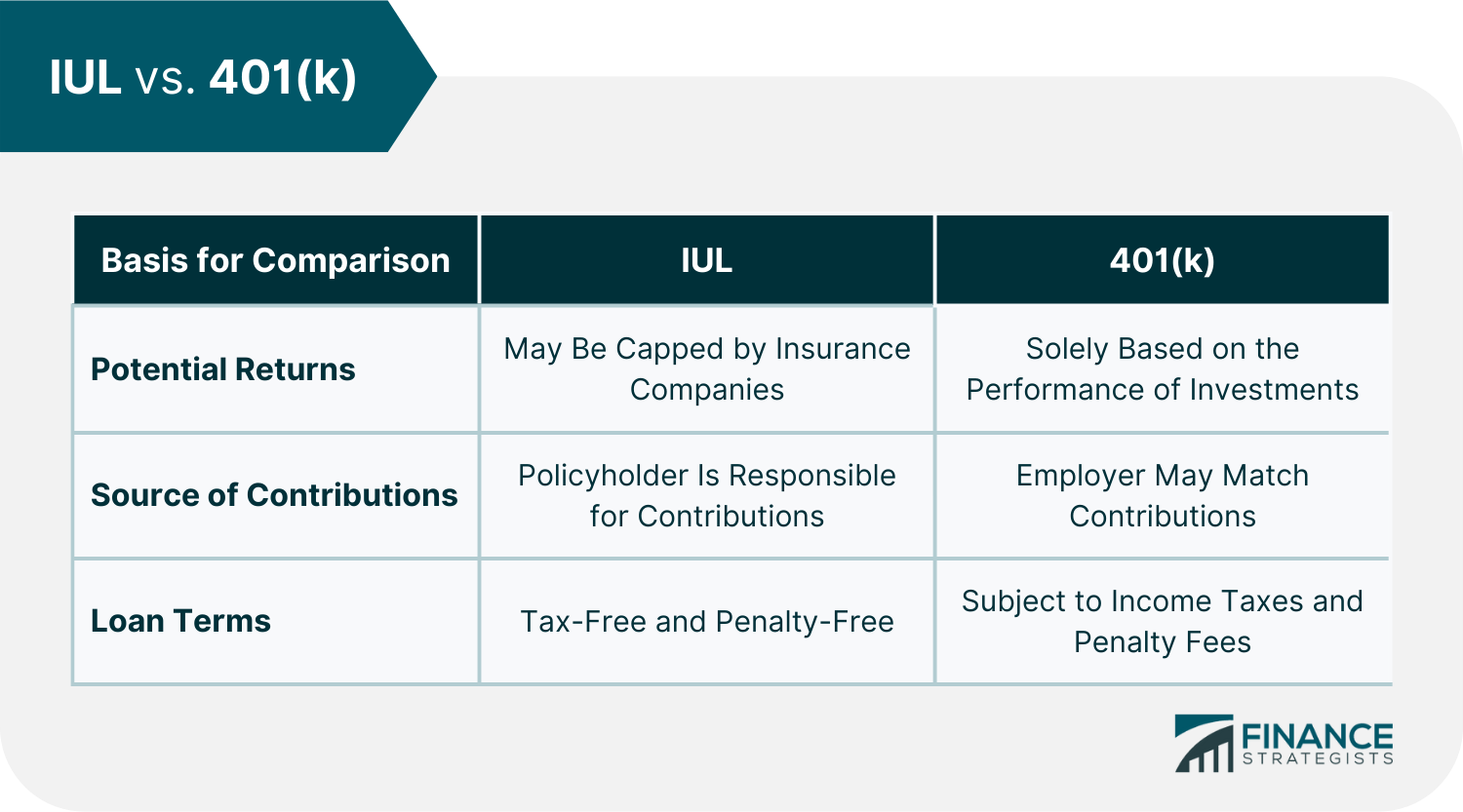

For the majority of people, no, IUL isn't much better than a 401(k) in regards to saving for retired life. A lot of IULs are best for high-net-worth people trying to find means to decrease their taxable earnings or those that have maxed out their various other retirement choices. For everyone else, a 401(k) is a better financial investment automobile since it doesn't lug the high fees and premiums of an IUL, plus there is no cap on the quantity you might make (unlike with an IUL policy).

While you might not lose any type of money in the account if the index goes down, you will not earn interest. If the marketplace transforms favorable, the profits on your IUL will certainly not be as high as a common investment account. The high cost of premiums and charges makes IULs pricey and considerably less economical than term life.

Indexed universal life (IUL) insurance policy provides cash money worth plus a survivor benefit. The cash in the money value account can make interest via tracking an equity index, and with some often alloted to a fixed-rate account. Indexed universal life plans cap how much money you can accumulate (usually at much less than 100%) and they are based on a perhaps unstable equity index.

Which Is Better Whole Life Or Universal Life

A 401(k) is a better option for that function due to the fact that it does not bring the high costs and costs of an IUL plan, plus there is no cap on the amount you might make when invested. Most IUL policies are best for high-net-worth people looking for to decrease their gross income. Investopedia does not supply tax obligation, investment, or financial solutions and guidance.

An independent insurance coverage broker can contrast all the alternatives and do what's finest for you. When comparing IUL quotes from various insurance policy companies, it can be complex and tough to recognize which alternative is best. An independent economic professional can clarify the different features and suggest the most effective alternative for your distinct situation.

Indexed Universal Life Leads

Instead of looking into all the various alternatives, calling insurance coverage companies, and asking for quotes, they do all the job for you. Lots of insurance coverage representatives are able to conserve their customers money due to the fact that they recognize all the ins and outs of Indexed Universal Life plans.

It's a credible company that was established in 1857 HQ lies in Milwaukee, offering for years in monetary services Among the largest insurer, with around 7.5% of the market share Has been serving its insurance policy holders for over 150 years. The company uses two kinds of offers that are term and long-term life policies.

For them, term life plans include persistent ailments, sped up death advantages, and ensured reimbursement alternatives. For a Common of Omaha life-indexed insurance policy, you require to have a quote or get in touch with a licensed representative.

Penn Mutual provides life insurance policies with various advantages that fit individuals's demands, like individuals's investment goals, economic markets, and spending plans. One more company that is renowned for providing index global life insurance plans is Nationwide.

Indexed Universal Life Cap Rates

The business's insurance policy's sturdiness is 10 to 30 years, along with the provided coverage to age 95. The business's global life insurance policies provide tax-free fatality benefits, tax-deferred incomes, and the versatility to adjust your costs repayments (insurance indexation).

You can likewise get kids's term insurance coverage and long-term treatment defense. If you are seeking among the top life insurance coverage firms, Pacific Life is a wonderful choice. The business has actually continuously gotten on the leading checklist of top IUL companies for several years in regards to selling products considering that the business established its really initial indexed global life products.

What's good concerning Lincoln Financial contrasted to other IUL insurer is that you can additionally transform term plans to global plans given your age is not over 70. Principal Financial insurance provider gives services to around 17 nations throughout global markets. The company provides term and global life insurance policy plans in all 50 states.

Variable universal life insurance policy can be taken into consideration for those still looking for a better alternative. The cash worth of an Indexed Universal Life policy can be accessed via policy lendings or withdrawals. Withdrawals will reduce the survivor benefit, and financings will certainly build up rate of interest, which should be repaid to keep the plan active.

Tax Free Retirement Iul

This policy style is for the client who needs life insurance policy however wish to have the ability to pick how their cash money value is invested. Variable plans are underwritten by National Life and distributed by Equity Solutions, Inc., Registered Broker/Dealer Associate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604.

The info and summaries had below are not planned to be complete descriptions of all terms, problems and exemptions relevant to the services and products. The exact insurance coverage under any COUNTRY Investors insurance policy item goes through the terms, conditions and exemptions in the real plans as provided. Products and services defined in this web site vary from one state to another and not all items, coverages or services are available in all states.

This details brochure is not a contract of insurance. The plan mentioned in this details pamphlet are safeguarded under the Plan Owners' Security System which is carried out by the Singapore Down Payment Insurance Corporation (SDIC).

To find out more on the kinds of advantages that are covered under the system along with the limits of protection, where relevant, please contact us or check out the Life Insurance Association, Singapore or SDIC internet sites () or (www.sdic.org.sg). This advertisement has actually not been reviewed by the Monetary Authority of Singapore.

{kind=link}

Latest Posts

Universal Life Insurance Cost Calculator

Wfg Iul

Guaranteed Universal Life Insurance Quotes